Creating a Savings Budget that works for you?

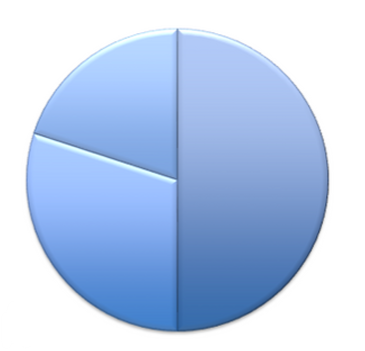

Setting and maintaining a personal budget has never been more important. With inflation driving up the cost of housing, groceries, and everyday essentials, many households are finding it harder to maintain the lifestyle they once had. A realistic budget helps you stay in control and plan for both today and the future. When creating a realistic budget, try to stick to the 50/30/20 Rule. 50% of total monthly income to be spent on essential expenses, 30% allocated to discretionary expenses, and 20% dedicated to savings.

1. Breakdown your monthly expenses

- Identify Total Monthly Income: Use your total take home (after tax) amount to determine your starting point.

- Identify essential expenses (50%): Mortgage or rent, insurance (including health, car, and property), groceries, utilities, transportation (car payment and gas), childcare, student loan repayments, credit card payments, etc.

- Add to cart! (30%): Everyone needs to reward themselves from time to time. Whether that’s ordering the coffee or going on that vacation you’ve been planning for years, be kind to yourself. Budgeting is not meant to be torture. It’s okay to indulge every now and again, just in moderation.

- Use this 20% for building an emergency fund, saving for retirement, and other financial goals. Many experts recommend contributing 12–15% of your income to retirement savings. If that feels overwhelming, start smaller (e.g., 5%) and increase by 1% each year until you reach your goal.

2. How to maintain your budget

- Track your budget using a spreadsheet or online tool – many financial institutions offer free, online templates that can be downloaded and used. Tracking your expenses each month is the best way to stay accountable and adjust as needed. Be sure to make your budgeting night fun! Reward yourself after updating your spreadsheet because you’re one month closer to your financial goals!

2. Finally, give yourself GRACE!

- It can take a few months to get this whole budgeting thing down and to feel comfortable with a new way of spending your money. Don’t be too hard on yourself, you’ll get it! If you need help figuring this out, reach out to your dedicated MCF financial advisor to schedule a complimentary meeting!

- What are your tools, and what’s in your Red Bucket? At the end of the day, the Big Red Bucket Theory is a simple way to understand the cause and effect of your financial choices.

You need to know:

- How much do you have in your retirement bucket?

- How much do you plan to take out?

- How many holes you might be adding along the way?

Here's the key question: How much money will you need to pull from that bucket throughout your retirement? We're talking about every dollar you'll spend, from groceries and gasoline to travel and health care.

That gives us two crucial numbers to work with:

- The amount in your big red bucket at retirement.

- The total amount you'll need to take out during your non-working years

IMPORTANT DISCLOSURE INFORMATION

MCF Advisors, LLC (“MCF”) is an SEC-registered investment adviser. Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by MCF), or any non-investment related content, made reference to directly or indirectly in this presentation will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this presentation serves as the receipt of, or as a substitute for, personalized investment advice from MCF. To the extent that a reader has any questions regarding the applicability of any specific issue discussed herein to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Information prepared from third-party sources is believed to be reliable though its accuracy is not guaranteed. MCF is neither a law firm nor a certified public accounting firm and no portion of the presentation content should be construed as legal or accounting advice. Information prepared from third-party sources is believed to be reliable though its accuracy is not guaranteed. A copy of MCF’s current written disclosure statement discussing our advisory services and fees is available upon request. If you are an MCF client, please remember to contact MCF in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing / evaluating / revising our previous recommendations and/or services. The scope of the services to be provided depends upon the needs of the client and the terms of the engagement.