Scanning the Horizon – Capital Markets

I am not surprised with the three-year 80%+ gain of the US equity market (SP 500)! Corporate profits and labor productivity gains were fairly well forecasted in our outlook from early June of 2022: we stated that inflation was transitory rather than structural (CPI hit a 9% annualized rate in May of 2022) and that once the Federal Reserve started withdrawing the excess fuel and increasing the price of fuel (fuel being the money supply and interest rates being the cost of fuel) that inflation would start it’s descent to the 2-3% level. We made assumptions that the pressure of wage increases were going to subside, consumers and corporations were in great financial shape due to the massive amount of liquidity injected into the system, and that Government spending would likely stay excessive, all contributing to an the economy that had lots of positive support rather than believe what most economists said: “we are headed into a recession”. As we noted at that time, “this is the most predicted recession that will never happen.” Wow, was that last statement ever more right!!!

Tariffs

Let’s speak to the 2025 noise during the spring and summer regarding tariffs being inflationary.

Recent concern about tariffs being structurally inflationary appears to be overstated. Tariffs function as a tax paid by consumers, creating a one‑time price increase rather than persistent inflation. Over time, higher prices suppress demand or encourage substitution, which is ultimately deflationary. While tariffs generate government revenue and temporarily benefit domestic producers, they can also reduce competitiveness if complacency develops. We expect inflation to continue declining through 2026.

US Equity Market

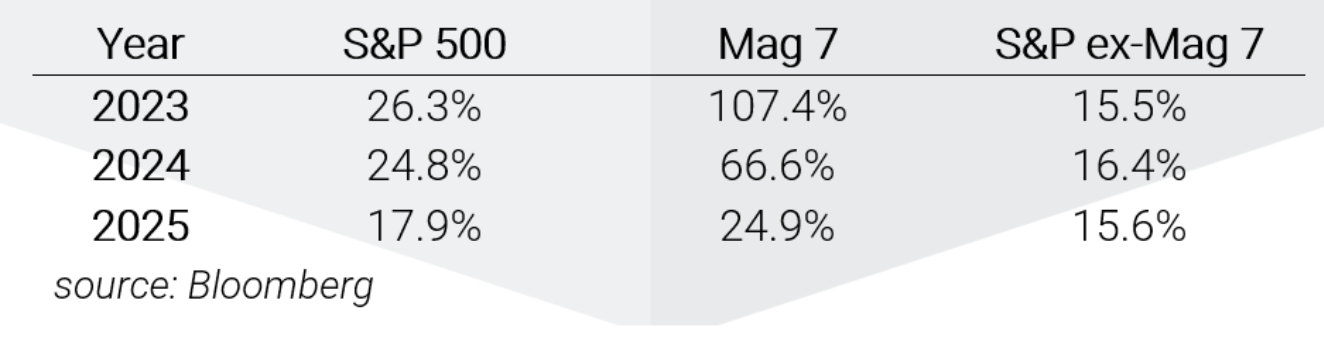

We have witnessed a massive spread between the Magnificent 7 (i.e. Mag 7 – Nvidia, Microsoft, Meta, Google, Apple, Amazon, Tesla) vs. the other 493 companies within the SP 500 Index. Below are annual total returns (price change plus dividends) for the S&P 500, Mag 7, and the S&P 500 excluding the Mag 7:

The Mag 7, representing 35% of the entire value of the 500 companies, is quite impressive. And perhaps even more impressive is that their earnings are 33% of the entire earnings of the SP 500 companies. So, who is to say that they might be ready to crash like the tech stock crash in 2000? Perhaps they deserve this weighting of the index?

Our view is that the leadership is about to change as the massive capital spending on AI technology will have dramatic effects on business growth and profits within the other 493 large companies within the 500 Index in addition to the small capitalize companies such as the S&P 600 Small Cap Index. The Mag 7 companies are focusing on out-running each another and even crossing over to the others’ space. Will this be a cannibalization of profits between the Kings? We are leaning to both changes happening (the other 493 and small companies outrunning the Mag 7 and cannibalization of the Mag 7 within their own).

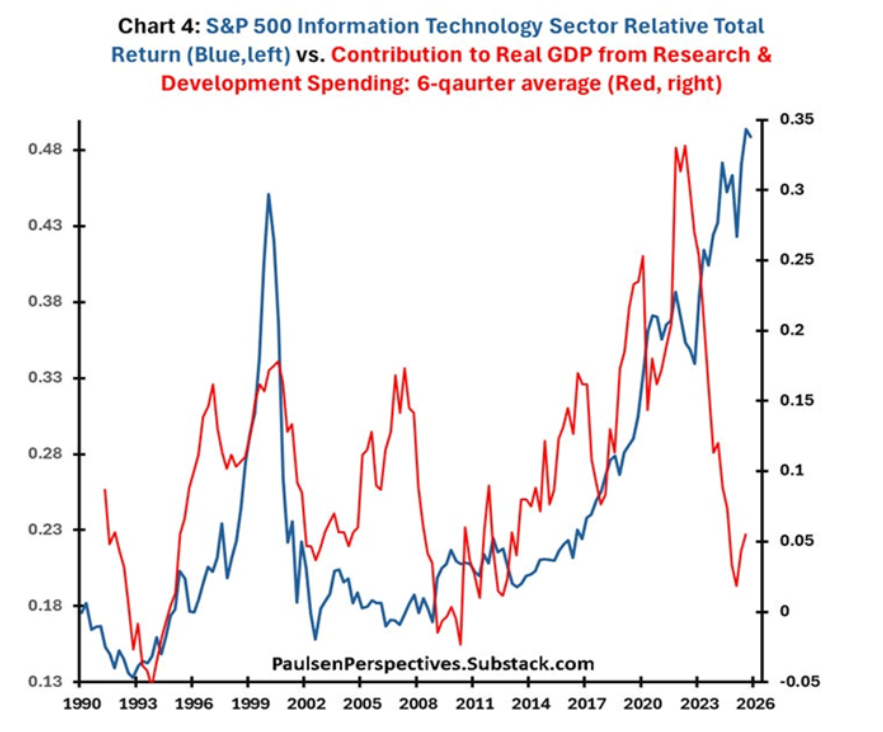

As you can see in the chart below, the R&D Spending as a % of GDP from the Tech Titans has dropped dramatically. Over the past 30-plus years this has been a good indicator that investment returns from the tech sector could be far less attractive than the non-tech sectors.

Thus, we have tilted away from a US Equity overweight from the Mag 7 to be more diversified to Large Cap Value (older line cyclical and finance companies) and Small Cap companies. While this is currently out of the mainstream action, we expect that in 2026 & 2027 this will be rewarded.

Monetary Policy

- Over a full business cycle (typical cycle lasts about 6-7 years for the past 150 years) the supply of money to the economic engine is very important. As a gasoline engine needs fuel but can run on its reserves for a while, there comes a time when a refueling is needed. Sometimes we inject way too much for the current need (the pandemic) and sometimes we restrict too much that the engine starts to sputter > current scenario.

- The price of the fuel (interest rates) is also very important. We anticipate the Fed to lower interest rates again in 2026, perhaps more than the market currently anticipates in Q2, 3 & 4.

- Banking reserves policies are being relaxed, thereby boosting the ability of banks to increase lending. This will add to the supply of money, further pressuring interest rates to ease, as supply wins over demand.

- Banking regulations are also being stripped from the previous administration’s agenda. By this very nature supporting improved bank profitability, which also enhances the bank’s ability and desire to make more loans, and thus again more supply and lower price of money.

- In our view, Fed Policy is still too restrictive:

- The current effective Fed Funds rate is 3.64% verses CPI of 2.5-3.0%, creating a negative real rate of interest of -0.64%. While it is better than four months ago when Fed Funds was 4.5% and CPI was at 3% = -1.50% real interest rate.

- June of 2026 the Federal reserve will start lowering the price of money (Fed Funds) and increasing the supply of money (Money Supply growth) at a much faster pace than the market currently anticipates. The reasons are two-fold:

- Trump is replacing the Fed Chairman in May with his pick, which will provide a direct influence to rev up the economy by pulling both of these levers.

- The economy is much like an aircraft carrier – it takes a while before it can turn around, meaning the economy is slowing and may get slower before the lower interest rates and increased money supply kick in. But by 2026 Q4 and 2027, we just might experience a significant boost from these monetary kickers, and most likely corporate profits the same and thus stock prices.

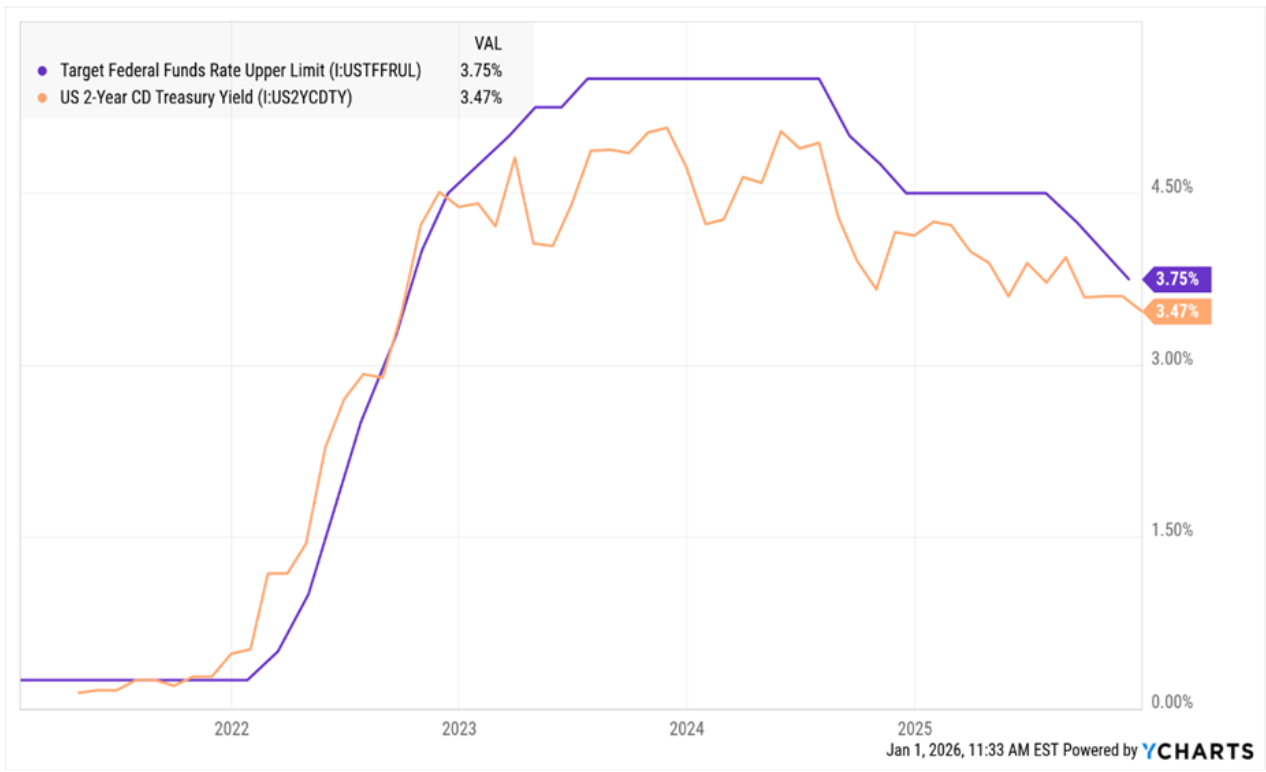

- The 2 Year US Treasury Note has been a directional predictor of the federal funds rate in recent years.

Labor

- Likely the supply will increase meaning an increase in the unemployment index.

- Economic growth has cooled down from the feverish pace of 2023-2024 and first part of 2025 putting less pressure on wage growth, and even the need, or lack thereof for more labor.

- In addition, AI has started the erosion of the labor force growth. Depending on the pace of AI adoption, we will likely experience a furthering of the spread between the “haves and the have nots”. I personally have some concerns that if the AI labor force growth rate erosion gets too magnified, we could see much unrest within the masses. I remember 50 years ago in the 70s when we had much social and economic turmoil, caused by the influx of my generation into the work-force and the social/economical viewpoints being challenged and changed. Perhaps this is an early warning sign that we must be thoughtful about our endgame > profits or people? Let’s do both with the viewpoint of “The Business of Business is People”.

Fiscal Policy

Many forecasters simply assume because deficit spending is so large, fiscal policy must be accommodative. However, fiscal policy has actually been contracting from about 7.3% deficit spending of the GDP in 2024 to only 5.2% currently. Looking into 2026, the recently restrictive fiscal policy (i.e. since the start of 2025, the federal deficit/GDP ratio has contracted) should weigh on overall real economic growth.

A Few Other Speed Bumps

- Possibility of another Government shutdown on Jan 30, 2026, as Congress only passed enough spending last fall to get us to end of January.

- Earnings growth stall may put a scare into the marketplace.

- Political and Policy Uncertainty as 2026 is a midterm election year, which historically brings increased market volatility and economic weakness. Unpredictable policy shifts, such as changes to tariffs or immigration rules, could cause disruption.

- Never ending Geopolitical Risks with Russia, China and who knows!

All this said, don’t be shaken out of your IP (investment policy) as we just might have a downside adjustment in stock prices during part of 2026, but quite possibly a solid finish and into 2027. What we must always be mindful of is that investment returns typically come in bunches and then un-bunch and then start another cycle. As Warren Buffett famously said, “I would rather have a bumpy 10% over time than a smooth 6%”.

Thanks for spending time reading. We welcome your outreach.

Dave Harris